The Cost of Certainty

Not making a decision is still a decision.

When it comes to money, choosing certainty or choosing to avoid making a decision altogether can quietly become one of the most expensive choices you ever make.

I see it regularly, cash balances building up over time, savings accounts that haven’t changed in years. Large amounts sitting idle because it feels safe, predictable, and controlled. No volatility. No surprises.

And on the surface, that makes sense. Nobody enjoys watching markets move around. Certainty feels comfortable.

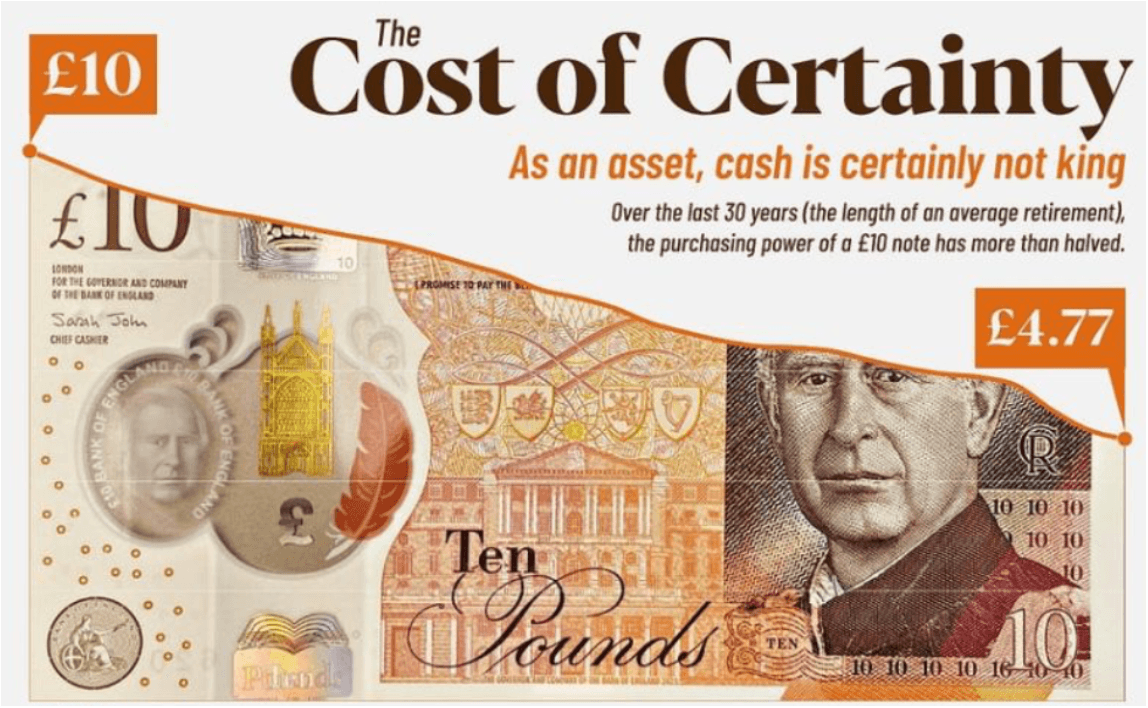

But here’s the uncomfortable reality: certainty has a cost. And that cost is inflation.

Inflation doesn’t feel dramatic, there’s no sudden crash or headline moment. Your bank balance doesn’t visibly drop. But slowly and consistently, the purchasing power of your money erodes. Prices rise, lifestyles become more expensive, and what used to feel like a comfortable amount of money gradually buys less and less.

Unlike market risk, inflation isn’t really optional. Markets might go up or down, Investments might perform better or worse than expected, but if your money isn’t growing faster than inflation, then in real terms you are losing ground.

“That’s why I often say inflation is the only flavour of risk that absolutely guarantees a loss in real terms.”

Cash absolutely has a role. Everyone should have liquidity. Life happens, emergencies arise, opportunities appear unexpectedly. As a general guide, somewhere around three to six months (depending on circumstances) worth of expenditure held in cash provides resilience and flexibility without compromising long-term progress. But beyond that excessive cash becomes a drag and it’s definitely not King.

If your money sits in low-return accounts for years while the cost of living rises, you are effectively locking in declining purchasing power. It doesn’t feel like a loss because the numbers don’t fall. But in real terms, the value is slowly shrinking.

That doesn’t mean everything should be invested either. Time horizon/Investment Term matters. Money that’s earmarked for a specific life event within the next five years, buying a property, relocating, funding education, or anything with a fixed timeline, usually shouldn’t be fully exposed to high levels of volatility.

But long-term money is different. If capital is intended for retirement, future lifestyle, or financial independence decades down the line, then leaving it sitting in cash or low-return assets can quietly do more damage than market volatility ever could.

Let me give you a simple example

Two people each start with £300,000.

One leaves their money sitting in cash. The balance doesn’t fluctuate. It feels safe and predictable. Twenty years later, they still have £300,000 on paper.

The second person receives proper financial planning and an education around market risk. Off the back of this conversation they are advised to invest in a globally diversified equity fund and achieves an annualised return of 9% per year, broadly in line with long-term global equity market returns.

After 20 years:

- The person who left their money in cash still has £300,000 nominally.

- The person who invested has approximately £1,680,000.

And that’s before you even considering inflation.

If inflation averaged 3% per year over that same period, the purchasing power of the original £300,000 would fall to roughly £166,000 in today’s money. So while one person believes they preserved wealth, in real terms they’ve lost almost half their buying power.

This is the cost of certainty.

Ready to Take the Next Step?

Everyone’s situation is different, and this isn’t to suggest that you need to chase returns or even invest at all. The purpose is simply to help you understand the real impact that rising prices of goods and services can have over time, and how money left idle in bank accounts may quietly lose purchasing power in real terms. The right strategy will always depend on your personal and financial circumstances, goals, and investment term. If you would like a full analysis of your current position and how inflation may affect your long-term plans, you can book a conversation with me here:

Enjoyed this article?

Get the next one delivered to your inbox.

Comments

Loading comments...

Related Articles

Continue reading more insights on financial planning.

Why Trying to Time the Market During Crises Rarely Works

Staying Calm During Uncertain Times: A Perspective for Investors in the Middle East