Investment Risk: The Risk Of Low Returns And Falling Short Of Your Financial Goals

When most people talk about investment risk, they usually mean volatility. They’re thinking about markets falling, picking the wrong stock, investing just before a crash, or missing out on the next big winner. But in my experience, that isn’t the biggest risk at all.

The biggest risk is misallocating your capital for decades.

And oddly enough, it often starts with a well-meaning risk questionnaire.

Categorised Before Being Educated

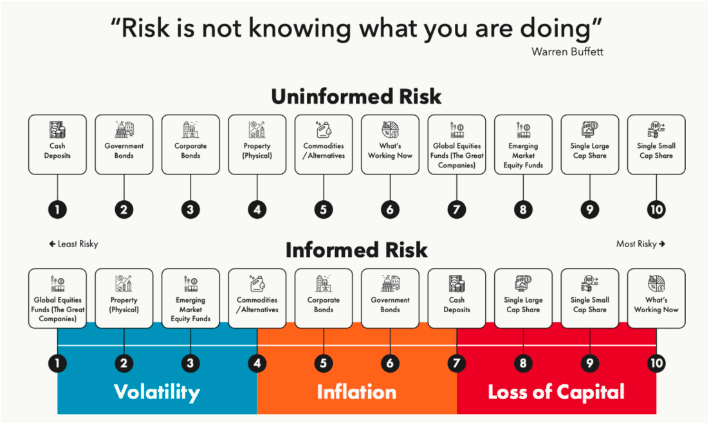

In many advisory processes, risk is determined by asking a series of questions about how you would feel if markets fell 10% or 20%. Whether you’d sell. Whether you prefer stability or growth. You answer honestly, usually cautiously and you’re labelled ‘cautious’, ‘moderate’ or ‘balanced’. From there, a portfolio is built that fits neatly into that category.

Don’t get me wrong, risk questionnaires do serve a purpose and the advisory profession has come a long way in terms of identifying investors behaviour. The problem is that most people are categorised before they’re educated.

Inexperienced investors haven’t yet been shown how markets actually behave over long periods. They haven’t seen how often downturns occur or how quickly and consistently they’ve recovered. They haven’t been walked through the maths of compounding. Instead, they’re asked how comfortable they are with something they don’t yet fully understand.

“That isn’t really advice; it’s administration.”

The Real Cost of Misallocation

A typical ‘balanced’ portfolio might be 50% equities and 50% bonds. It feels sensible. It feels responsible. But if someone has a 20–30 year investment term, which most retirement investors do, the greater risk is not volatility at all; it’s insufficient growth.

Let’s make this tangible. Imagine two investors, each starting with £500,000 and investing for 25 years without adding or withdrawing anything. One invests entirely in global equities. The other splits the money 50/50 between equities and bonds. Using conservative long-term assumptions, say 9% a year for equities and 4% for bonds:

- The fully invested equity portfolio grows to roughly £4.3 million over 25 years.

- The 50/50 portfolio grows to around £2.4 million.

That’s a £1.9 million difference. Not because one investor picked better funds. Not because one timed the market perfectly. Simply because of allocation and the power of compounding and not being properly educated around risk prior to investing.

Allocation Should Be Driven by Objectives

Now, to be absolutely clear, this is not me suggesting everyone should be 100% in equities. That would be lazy advice. Asset allocation has to reflect time horizon, income needs, liquidity requirements and, importantly, behavioural temperament.

If someone needs their capital in three to five years, high equity exposure may be entirely inappropriate. If someone genuinely cannot tolerate drawdowns, forcing them into a volatile portfolio will likely lead to poor decisions at the worst possible time.

The point isn’t that equities are ‘good’ and bonds are ‘bad’. The point is that allocation should be driven by objectives and time horizon — not just by discomfort with short-term market movements.

The Declines Are Temporary, The Advance Is Permanent

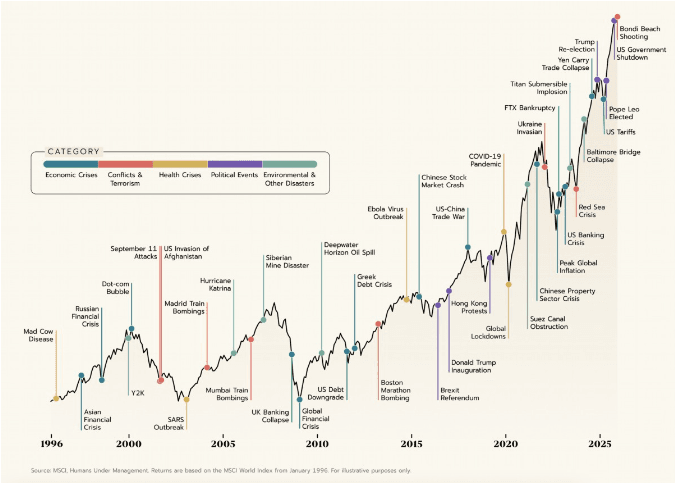

When you zoom out and look at history, global equity markets have endured world wars, depressions, oil crises, financial collapses and pandemics. They have fallen sharply at times, sometimes painfully so, but they have never remained down permanently. Over sufficiently long periods, diversified global markets have always recovered and progressed higher.

That doesn’t mean declines don’t happen. They do. It doesn’t mean volatility disappears. It won’t. But there is a fundamental difference between volatility and permanent loss. Volatility is temporary price movement. Permanent loss is capital that never recovers. Historically, long-term investors in diversified global equities have experienced the former.

“What tends to create permanent damage isn’t the market itself; it’s behaviour. Selling during downturns. Abandoning strategy mid-cycle. Staying overly defensive for decades because short-term declines feel uncomfortable.”

The best portfolio will always be the one you stick to.

The Inflation Dimension

Inflation adds another dimension that often gets overlooked. At around 3% inflation, purchasing power roughly halves every 24 years. A portfolio that feels ‘safe’ but grows too slowly can quietly erode future lifestyle options. That risk rarely appears in a questionnaire, but it’s very real.

So What Is Investment Risk, Really?

It’s failing to achieve your lifetime objectives because your capital was structured incorrectly, or because you reacted emotionally, doing the wrong thing at the wrong time.

Context matters. Education matters. Behaviour matters more than most people realise.

People don’t come to advisers to be labelled ‘moderate’. They come for clarity. They come to understand how markets work, what normal volatility looks like and how their money needs to behave in order to support their life.

Ready for a Proper Conversation About Your Money?

A proper advisory process starts with education, not categorisation. If you’d like to understand how your capital should be structured to support your long-term goals, you’re welcome to book a confidential discovery meeting.

No pressure, no obligation — just a conversation about where you are today, what you want to achieve, and whether your current strategy truly supports your future.

Enjoyed this article?

Get the next one delivered to your inbox.

Comments

Loading comments...

Related Articles

Continue reading more insights on financial planning.

Why Trying to Time the Market During Crises Rarely Works

Staying Calm During Uncertain Times: A Perspective for Investors in the Middle East